import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from matplotlib.pyplot import subplots1. imports

import statsmodels.api as sm

from statsmodels.stats.outliers_influence import variance_inflation_factor as VIF

from statsmodels.stats.anova import anova_lmfrom ISLP import load_data2. 단순 선형 회귀 분석

- Boston data 불러오기

- lstat 변수만 사용

- X = [1,

lstat벡터] 형태 - y = medv 변수

from ISLP.models import (ModelSpec as MS, summarize , poly)

from pandas.io.formats.format import DataFrameFormatter

# Inside the pandas/io/formats/html.py file (you'll need to find this file in your pandas installation),

# locate the _get_columns_formatted_values function and modify it as follows:

def _get_columns_formatted_values(self) -> list[str]:

# only reached with non-Multi Index

# return self.columns._format_flat(include_name=False) # Replace this line

formatter = DataFrameFormatter(self.columns, include_name=False) # With this line

return formatter._format_col_name_split()

Boston = load_data("Boston")

print(Boston.columns)

X = pd.DataFrame({'intercept': np.ones(Boston.shape[0]), 'lstat': Boston['lstat']})

print(X[:4])

y = Boston['medv']

print(f'-데이터의 수 : {len(y)}')Index(['crim', 'zn', 'indus', 'chas', 'nox', 'rm', 'age', 'dis', 'rad', 'tax',

'ptratio', 'lstat', 'medv'],

dtype='object')

intercept lstat

0 1.0 4.98

1 1.0 9.14

2 1.0 4.03

3 1.0 2.94

-데이터의 수 : 506- Boston data 단순 선형 회귀 분석

- medv ~ lstat

- \(R^2\) 독립변수가 종속변수를 얼마나 잘 설명하는지 0~1사이

- 독립변수가 늘어날수록 무조건 증가

- adj. \(R^2\) 변수의 수를 고려해 보정 (단순 선형 회귀에서는 거의 같음)

- DF(Degrees of Freedom, 자유도) 1/504

- DF Residuals : 504 \(\to\) 잔차 자유도(관측값 수 - 추정한 모수 수-보통 n-2)

- DF Model : 1 \(\to\) 회귀 자유도(독립변수 수)

- Durbin-Watson(DW 통계량) : 오차들 사이에 자기상관

- 2 근처 : 자기상관 없음(좋음)

- 2보다 작음 : 양의 자기상관

- 2보다 큼 : 음의 자기상관

- Skew : 왜도

- 0 : 완전 대칭

- (> 0) : 오른쪽 꼬리가 길다

- (< 0 ) : 왼쪽 꼬리가 길다

- Kurtosis : 첨도

- 3 : 정규분포

- (> 3) : 뾰족하고 꼬리가 두꺼움

- (< 3) : 평평하고 꼬리가 얇음

- 덜 중요?

- F-statistic : 전체 모델이 통계적으로 유의미한지

- Prob : F값에 따른 p-value

- intercept : 절편

- coef : lstat = 0 일 때 medv가 34.55로 예측된다는 뜻

- std err : 표준오차

- t : t-통계량 \(\to\) 계수가 0인지 아닌지 검정

- P>|t| : p-value \(\to\) 작을수록 유의미한 변수

- [0.025, 0.975] : 95% 신뢰구간

- lstat

- coef : lstat이 1% 증가할 때 medv는 약 0.95감소

- Omnibus : 정규성 검정 \(\to\) 클수록 정규성 위배 가능성 커짐

- Prob(Omnibus) : p-value 0.000 이므로 정규분포 아닐 가능성 큼

- Jarque-Bera : 또다른 정규성 검정 지표

- Log-Likelihood : 모델의 로그 가능도

- AIC / BIC : 모형 간 비교 지표(낮을 수록 좋음)

- Cond. No : 다중공선성 지표(높으면 위험)

model = sm.OLS(y, X)

results = model.fit()

print(results.summary()) OLS Regression Results

==============================================================================

Dep. Variable: medv R-squared: 0.544

Model: OLS Adj. R-squared: 0.543

Method: Least Squares F-statistic: 601.6

Date: Sun, 06 Apr 2025 Prob (F-statistic): 5.08e-88

Time: 09:10:46 Log-Likelihood: -1641.5

No. Observations: 506 AIC: 3287.

Df Residuals: 504 BIC: 3295.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

intercept 34.5538 0.563 61.415 0.000 33.448 35.659

lstat -0.9500 0.039 -24.528 0.000 -1.026 -0.874

==============================================================================

Omnibus: 137.043 Durbin-Watson: 0.892

Prob(Omnibus): 0.000 Jarque-Bera (JB): 291.373

Skew: 1.453 Prob(JB): 5.36e-64

Kurtosis: 5.319 Cond. No. 29.7

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.- _X : 아무런 변수 생성 : p-value 0.05보다 작게 나올수도?

- T-test로 변수 선택하는데에는 한계 존재, 변수가 많을 때는 다른 방법

_X =np.random.normal(0,1, size=(len(y), len(y-1)))

_Xarray([[-1.2014418 , -0.36229144, -0.20156353, ..., 0.5128146 ,

-1.69055217, 1.36297382],

[ 1.97238504, -0.22323065, 0.51710176, ..., 0.81227357,

-0.85792917, 0.27368867],

[-0.74635151, -0.2920941 , -0.8552335 , ..., 1.22772083,

-0.07547889, -0.59557387],

...,

[ 0.20602294, 0.13454536, 0.72263167, ..., 0.03738331,

0.49048762, -0.44020111],

[-0.07030914, -0.04136855, 0.16204887, ..., 0.23999928,

1.4415386 , 0.69481763],

[ 0.30221035, -0.50379848, -0.81854603, ..., 0.47187981,

-0.95241703, 0.0196086 ]])- MS 구문 이용해 입력 행렬 처리

design = MS(['lstat'])

design = design.fit(Boston)

X = design.transform(Boston)

print(X[:4])

model = sm.OLS(y, X)

results = model.fit()

print(results.params) intercept lstat

0 1.0 4.98

1 1.0 9.14

2 1.0 4.03

3 1.0 2.94

intercept 34.553841

lstat -0.950049

dtype: float64- 새로운 입력변수 [1 , lstat벡터] 생성, 예측

new_df = pd.DataFrame({'lstat':[5, 10, 15]})

newX = design.transform(new_df)

print(newX)

new_predictions = results.get_prediction(newX);

print(f'평균 : \n{new_predictions.predicted_mean}')

print(f'신뢰구간 : \n{new_predictions.conf_int(alpha=0.05)}')

print(f'예측구간 : \n{new_predictions.conf_int(obs=True, alpha=0.05)}') intercept lstat

0 1.0 5

1 1.0 10

2 1.0 15

평균 :

[29.80359411 25.05334734 20.30310057]

신뢰구간 :

[[29.00741194 30.59977628]

[24.47413202 25.63256267]

[19.73158815 20.87461299]]

예측구간 :

[[17.56567478 42.04151344]

[12.82762635 37.27906833]

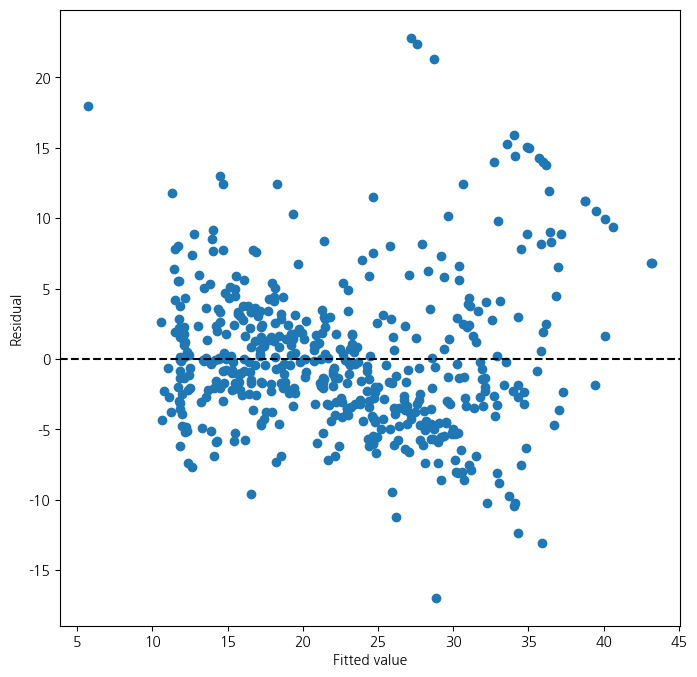

[ 8.0777421 32.52845905]]- 평균직선에 대한 그래프 / 잔차에 대한 그래프

import matplotlib.pyplot as plt

def abline(ax, b, m):

xlim = ax.get_xlim()

ylim = [m * xlim[0] + b, m * xlim[1] + b]

ax.plot(xlim, ylim)

def abline(ax, b, m, *args, **kwargs):

xlim = ax.get_xlim()

ylim = [m * xlim[0] + b, m * xlim[1] + b]

ax.plot(xlim, ylim, *args, **kwargs)

ax = subplots(figsize=(5,5))[1]

abline(ax,

results.params[0],

results.params[1], 'r--', linewidth=3)

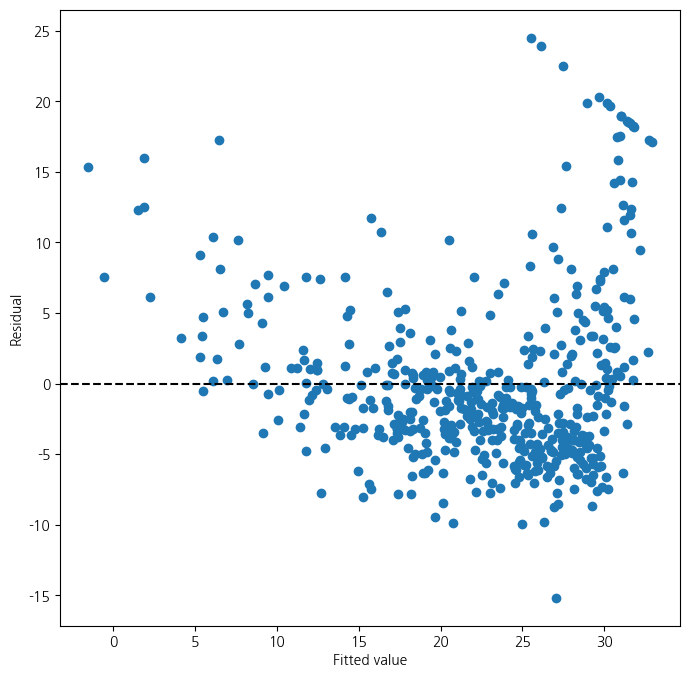

ax = subplots(figsize=(8,8))[1]

ax.scatter(results.fittedvalues, results.resid)

ax.set_xlabel('Fitted value')

ax.set_ylabel('Residual')

ax.axhline(0, c='k', ls='--');/tmp/ipykernel_147714/1347888005.py:15: FutureWarning: Series.__getitem__ treating keys as positions is deprecated. In a future version, integer keys will always be treated as labels (consistent with DataFrame behavior). To access a value by position, use `ser.iloc[pos]`

results.params[0],

/tmp/ipykernel_147714/1347888005.py:16: FutureWarning: Series.__getitem__ treating keys as positions is deprecated. In a future version, integer keys will always be treated as labels (consistent with DataFrame behavior). To access a value by position, use `ser.iloc[pos]`

results.params[1], 'r--', linewidth=3)

- 잔차 표준화 필요 : 0~1사이 왔다갔다..

- 현재 문제점 : 잔차들이 곡선의 형태를 띄고 있음 \(\to\) 곡선을 표현할 수 있는 변수 사용

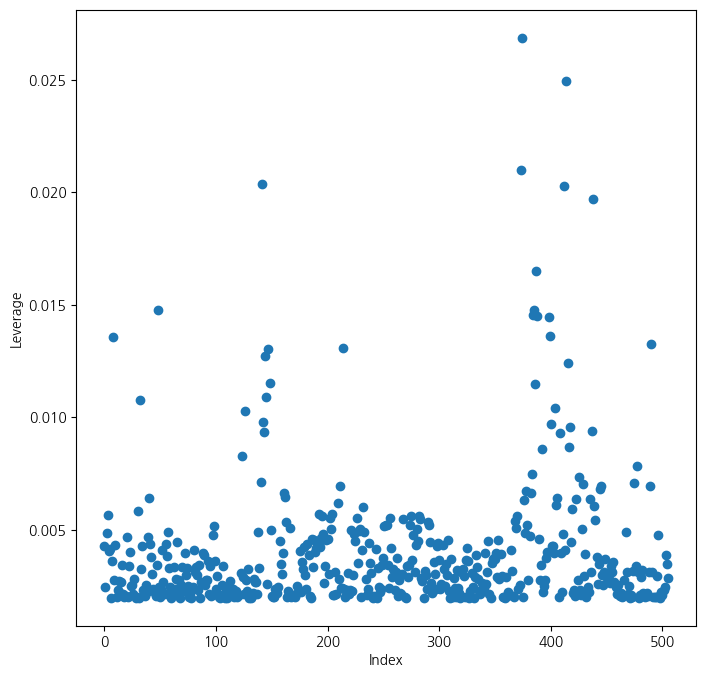

- 관측치에 대한 leverage(각 관측치의 영향력) 계산 및 그래프화

- 각 데이터마다 영향의 크기가 다름

infl = results.get_influence()

ax = subplots(figsize=(8,8))[1]

ax.scatter(np.arange(X.shape[0]), infl.hat_matrix_diag)

ax.set_xlabel('Index')

ax.set_ylabel('Leverage')

np.argmax(infl.hat_matrix_diag)374

3. 다중 선형 회귀

- 입력 변수를 lstat + age로 변경

X = MS(['lstat', 'age']).fit_transform(Boston)

model1 = sm.OLS(y, X)

results1 = model1.fit()

print(summarize(results1)) coef std err t P>|t|

intercept 33.2228 0.731 45.458 0.000

lstat -1.0321 0.048 -21.416 0.000

age 0.0345 0.012 2.826 0.005- 입력변수를 mdev를 제외한 모든 변수로 확장

terms = Boston.columns.drop('medv')

terms

X = MS(terms).fit_transform(Boston)

model = sm.OLS(y, X)

results = model.fit()

print(summarize(results)) coef std err t P>|t|

intercept 41.6173 4.936 8.431 0.000

crim -0.1214 0.033 -3.678 0.000

zn 0.0470 0.014 3.384 0.001

indus 0.0135 0.062 0.217 0.829

chas 2.8400 0.870 3.264 0.001

nox -18.7580 3.851 -4.870 0.000

rm 3.6581 0.420 8.705 0.000

age 0.0036 0.013 0.271 0.787

dis -1.4908 0.202 -7.394 0.000

rad 0.2894 0.067 4.325 0.000

tax -0.0127 0.004 -3.337 0.001

ptratio -0.9375 0.132 -7.091 0.000

lstat -0.5520 0.051 -10.897 0.000- p-value가 가장 높은 indus, age 변수 제외

minus_age = Boston.columns.drop(['medv','indus', 'age'])

Xma = MS(minus_age).fit_transform(Boston)

model1 = sm.OLS(y, Xma)

print(summarize(model1.fit())) coef std err t P>|t|

intercept 41.4517 4.903 8.454 0.000

crim -0.1217 0.033 -3.696 0.000

zn 0.0462 0.014 3.378 0.001

chas 2.8719 0.863 3.329 0.001

nox -18.2624 3.565 -5.122 0.000

rm 3.6730 0.409 8.978 0.000

dis -1.5160 0.188 -8.078 0.000

rad 0.2839 0.064 4.440 0.000

tax -0.0123 0.003 -3.608 0.000

ptratio -0.9310 0.130 -7.138 0.000

lstat -0.5465 0.047 -11.519 0.000- 변수 제외하고 중간에서도 전체 요약을 출력해 전체적인 변화를 봐야함

result1 = model1.fit()

#print(result1.summary())- 다중공선성을 확인하기 위한 VIF값

- 값이 크다는 것은 \(R^2\)가 크다는 것

- \(\to\) 자신이 없어도 나머지 변수들의 영향을 많이 받아 설명을 잘한다는 의미

vals = [VIF(X, i) for i in range(1, X.shape[1])]

vif = pd.DataFrame({'vif':vals},index=X.columns[1:])

print(vif) vif

crim 1.767486

zn 2.298459

indus 3.987181

chas 1.071168

nox 4.369093

rm 1.912532

age 3.088232

dis 3.954037

rad 7.445301

tax 9.002158

ptratio 1.797060

lstat 2.870777- 교호작용을 포함한 선형회귀분석

- 교호작용이라는 두 변수 간의 시너지 존재하는 경우!

- 특정 변수가 다른 변수의 영향력에 영향을 준다는 의미

- 변수가 많으면 모든 교호작용 고려 힘듦

- EDA먼저 필요

- lstat과 age간의교호작용

- 결과 :

lstat이 평균을 높여주는 효과가age가 클수록 커짐

X = MS(['lstat', 'age', ('lstat', 'age')]).fit_transform(Boston)

model2 = sm.OLS(y, X)

print(summarize(model2.fit())) coef std err t P>|t|

intercept 36.0885 1.470 24.553 0.000

lstat -1.3921 0.167 -8.313 0.000

age -0.0007 0.020 -0.036 0.971

lstat:age 0.0042 0.002 2.244 0.025- lstat에 대해 다항식 차원을 2까지 늘림

- lstat + lstat\(^2\)

- 만약 5차원이면 lstat + lstat\(^2\) + … + lstat\(^5\)

- 아래에서 2차식까지 통계적 유의성 확인됨

X = MS([poly('lstat', degree=2), 'age']).fit_transform(Boston)

model3 = sm.OLS(y, X)

results3 = model3.fit()

print(summarize(results3)) coef std err t P>|t|

intercept 17.7151 0.781 22.681 0.0

poly(lstat, degree=2)[0] -179.2279 6.733 -26.620 0.0

poly(lstat, degree=2)[1] 72.9908 5.482 13.315 0.0

age 0.0703 0.011 6.471 0.0- result1은 lstat에 대한 선형, result3은 lstat에 대한 2차 다항식

- 아래 검정은 다항식을 2차로 쓰는 것이 유의한지를 검정

- 0,1 둘 다 유의하다는 결과 \(\to\) 그러면 2차식까지 쓰는 것이 맞음

- 큰 모형에서 확실한 효과가 있다는 것이 보여짐

print(anova_lm(results1, results3)) df_resid ssr df_diff ss_diff F Pr(>F)

0 503.0 19168.128609 0.0 NaN NaN NaN

1 502.0 14165.613251 1.0 5002.515357 177.278785 7.468491e-35- results3의 결과에 대한 잔차의 산점도

ax = subplots(figsize=(8,8))[1]

ax.scatter(results3.fittedvalues, results3.resid)

ax.set_xlabel('Fitted value')

ax.set_ylabel('Residual')

ax.axhline(0, c='k', ls='--')

- Carseats data

Sales반응변수- 나머지 전체 +

IncomeAdvertising과PriceAge의 교호작용 추가 - 둘 중에서

Income*advertising만 통계적으로 유의

Carseats = load_data('Carseats')

print(Carseats.columns)

print(Carseats.head())

allvars = list(Carseats.columns.drop('Sales'))

y = Carseats['Sales']

final = allvars + [('Income', 'Advertising'),('Price', 'Age')]

X = MS(final).fit_transform(Carseats)

model = sm.OLS(y, X)

print(model.fit().aic)

print(summarize(model.fit()))Index(['Sales', 'CompPrice', 'Income', 'Advertising', 'Population', 'Price',

'ShelveLoc', 'Age', 'Education', 'Urban', 'US'],

dtype='object')

Sales CompPrice Income Advertising Population Price ShelveLoc Age \

0 9.50 138 73 11 276 120 Bad 42

1 11.22 111 48 16 260 83 Good 65

2 10.06 113 35 10 269 80 Medium 59

3 7.40 117 100 4 466 97 Medium 55

4 4.15 141 64 3 340 128 Bad 38

Education Urban US

0 17 Yes Yes

1 10 Yes Yes

2 12 Yes Yes

3 14 Yes Yes

4 13 Yes No

1157.337779308029

coef std err t P>|t|

intercept 6.5756 1.009 6.519 0.000

CompPrice 0.0929 0.004 22.567 0.000

Income 0.0109 0.003 4.183 0.000

Advertising 0.0702 0.023 3.107 0.002

Population 0.0002 0.000 0.433 0.665

Price -0.1008 0.007 -13.549 0.000

ShelveLoc[Good] 4.8487 0.153 31.724 0.000

ShelveLoc[Medium] 1.9533 0.126 15.531 0.000

Age -0.0579 0.016 -3.633 0.000

Education -0.0209 0.020 -1.063 0.288

Urban[Yes] 0.1402 0.112 1.247 0.213

US[Yes] -0.1576 0.149 -1.058 0.291

Income:Advertising 0.0008 0.000 2.698 0.007

Price:Age 0.0001 0.000 0.801 0.4244. 가변수 사용법

from ISLP.models import contrast

Bike = load_data('Bikeshare')

Bike.shape, Bike.columns((8645, 15),

Index(['season', 'mnth', 'day', 'hr', 'holiday', 'weekday', 'workingday',

'weathersit', 'temp', 'atemp', 'hum', 'windspeed', 'casual',

'registered', 'bikers'],

dtype='object'))X2 = MS(['mnth', 'hr', 'workingday','temp', 'weathersit']).fit_transform(Bike)

Y = Bike['bikers']

M1_lm = sm.OLS(Y, X2).fit()

S2 = summarize(M1_lm)

print(S2) coef std err t P>|t|

intercept -68.6317 5.307 -12.932 0.000

mnth[Feb] 6.8452 4.287 1.597 0.110

mnth[March] 16.5514 4.301 3.848 0.000

mnth[April] 41.4249 4.972 8.331 0.000

mnth[May] 72.5571 5.641 12.862 0.000

mnth[June] 67.8187 6.544 10.364 0.000

mnth[July] 45.3245 7.081 6.401 0.000

mnth[Aug] 53.2430 6.640 8.019 0.000

mnth[Sept] 66.6783 5.925 11.254 0.000

mnth[Oct] 75.8343 4.950 15.319 0.000

mnth[Nov] 60.3100 4.610 13.083 0.000

mnth[Dec] 46.4577 4.271 10.878 0.000

hr[1] -14.5793 5.699 -2.558 0.011

hr[2] -21.5791 5.733 -3.764 0.000

hr[3] -31.1408 5.778 -5.389 0.000

hr[4] -36.9075 5.802 -6.361 0.000

hr[5] -24.1355 5.737 -4.207 0.000

hr[6] 20.5997 5.704 3.612 0.000

hr[7] 120.0931 5.693 21.095 0.000

hr[8] 223.6619 5.690 39.310 0.000

hr[9] 120.5819 5.693 21.182 0.000

hr[10] 83.8013 5.705 14.689 0.000

hr[11] 105.4234 5.722 18.424 0.000

hr[12] 137.2837 5.740 23.916 0.000

hr[13] 136.0359 5.760 23.617 0.000

hr[14] 126.6361 5.776 21.923 0.000

hr[15] 132.0865 5.780 22.852 0.000

hr[16] 178.5206 5.772 30.927 0.000

hr[17] 296.2670 5.749 51.537 0.000

hr[18] 269.4409 5.736 46.976 0.000

hr[19] 186.2558 5.714 32.596 0.000

hr[20] 125.5492 5.704 22.012 0.000

hr[21] 87.5537 5.693 15.378 0.000

hr[22] 59.1226 5.689 10.392 0.000

hr[23] 26.8376 5.688 4.719 0.000

workingday 1.2696 1.784 0.711 0.477

temp 157.2094 10.261 15.321 0.000

weathersit[cloudy/misty] -12.8903 1.964 -6.562 0.000

weathersit[heavy rain/snow] -109.7446 76.667 -1.431 0.152

weathersit[light rain/snow] -66.4944 2.965 -22.425 0.000- contrast : 범주형 변수에 대한 코딩방식 지정

sum은 범주혀 변수의 모든 계수의 합이 0이 되도록 제약- 그러면 마지막 범주는 계수 추정되지 않고 나머지 계수들의 합의 음수가 됨

- 결과가 0에 가까움 \(\to\) 거의 차이가 없음, 예측력 자체는 인코딩 방식에 거의 영향을 받지 않음

hr_encode = contrast('hr', 'sum') # 합에 대한 제약을 검

mnth_encode = contrast('mnth', 'sum') # 합에 대한 제약을 검

X2 = MS([mnth_encode, hr_encode, 'workingday','temp', 'weathersit']).fit_transform(Bike)

Y = Bike['bikers']

M2_lm = sm.OLS(Y, X2).fit()

S2 = summarize(M2_lm)

print(S2)

np.sum((M1_lm.fittedvalues - M2_lm.fittedvalues)**2) coef std err t P>|t|

intercept 73.5974 5.132 14.340 0.000

mnth[Jan] -46.0871 4.085 -11.281 0.000

mnth[Feb] -39.2419 3.539 -11.088 0.000

mnth[March] -29.5357 3.155 -9.361 0.000

mnth[April] -4.6622 2.741 -1.701 0.089

mnth[May] 26.4700 2.851 9.285 0.000

mnth[June] 21.7317 3.465 6.272 0.000

mnth[July] -0.7626 3.908 -0.195 0.845

mnth[Aug] 7.1560 3.535 2.024 0.043

mnth[Sept] 20.5912 3.046 6.761 0.000

mnth[Oct] 29.7472 2.700 11.019 0.000

mnth[Nov] 14.2229 2.860 4.972 0.000

hr[0] -96.1420 3.955 -24.307 0.000

hr[1] -110.7213 3.966 -27.916 0.000

hr[2] -117.7212 4.016 -29.310 0.000

hr[3] -127.2828 4.081 -31.191 0.000

hr[4] -133.0495 4.117 -32.319 0.000

hr[5] -120.2775 4.037 -29.794 0.000

hr[6] -75.5424 3.992 -18.925 0.000

hr[7] 23.9511 3.969 6.035 0.000

hr[8] 127.5199 3.950 32.284 0.000

hr[9] 24.4399 3.936 6.209 0.000

hr[10] -12.3407 3.936 -3.135 0.002

hr[11] 9.2814 3.945 2.353 0.019

hr[12] 41.1417 3.957 10.397 0.000

hr[13] 39.8939 3.975 10.036 0.000

hr[14] 30.4940 3.991 7.641 0.000

hr[15] 35.9445 3.995 8.998 0.000

hr[16] 82.3786 3.988 20.655 0.000

hr[17] 200.1249 3.964 50.488 0.000

hr[18] 173.2989 3.956 43.806 0.000

hr[19] 90.1138 3.940 22.872 0.000

hr[20] 29.4071 3.936 7.471 0.000

hr[21] -8.5883 3.933 -2.184 0.029

hr[22] -37.0194 3.934 -9.409 0.000

workingday 1.2696 1.784 0.711 0.477

temp 157.2094 10.261 15.321 0.000

weathersit[cloudy/misty] -12.8903 1.964 -6.562 0.000

weathersit[heavy rain/snow] -109.7446 76.667 -1.431 0.152

weathersit[light rain/snow] -66.4944 2.965 -22.425 0.0001.6273003592224878e-19- 제약조건이 걸린 계수 확인

- 위의 계수들의 합에 음수를 취해 마지막 계수 생성

coef_month = S2[S2.index.str.contains('mnth')]['coef']

print(coef_month)

months = Bike['mnth'].dtype.categories

coef_month = pd.concat([coef_month, pd.Series([-coef_month.sum()], index=['mnth[Dec]'])

])

print(coef_month)mnth[Jan] -46.0871

mnth[Feb] -39.2419

mnth[March] -29.5357

mnth[April] -4.6622

mnth[May] 26.4700

mnth[June] 21.7317

mnth[July] -0.7626

mnth[Aug] 7.1560

mnth[Sept] 20.5912

mnth[Oct] 29.7472

mnth[Nov] 14.2229

Name: coef, dtype: float64

mnth[Jan] -46.0871

mnth[Feb] -39.2419

mnth[March] -29.5357

mnth[April] -4.6622

mnth[May] 26.4700

mnth[June] 21.7317

mnth[July] -0.7626

mnth[Aug] 7.1560

mnth[Sept] 20.5912

mnth[Oct] 29.7472

mnth[Nov] 14.2229

mnth[Dec] 0.3705

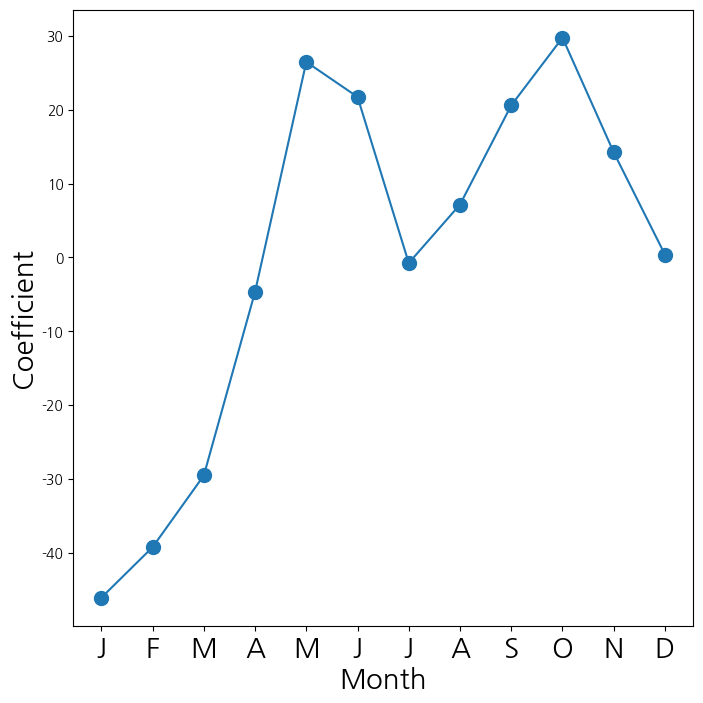

dtype: float64- 월에 대응되는 계수들을 선도표로 연결해서 시각화

- 겨울에는 잘 안타는 듯

- 여름에도 조금 떨어지는 경향을 보임

fig_month , ax_month = subplots(figsize=(8,8))

x_month = np.arange(coef_month.shape[0])

ax_month.plot(x_month , coef_month , marker='o', ms=10)

ax_month.set_xticks(x_month)

ax_month.set_xticklabels([l[5] for l in coef_month.index], fontsize

=20)

ax_month.set_xlabel('Month', fontsize=20)

ax_month.set_ylabel('Coefficient', fontsize=20);

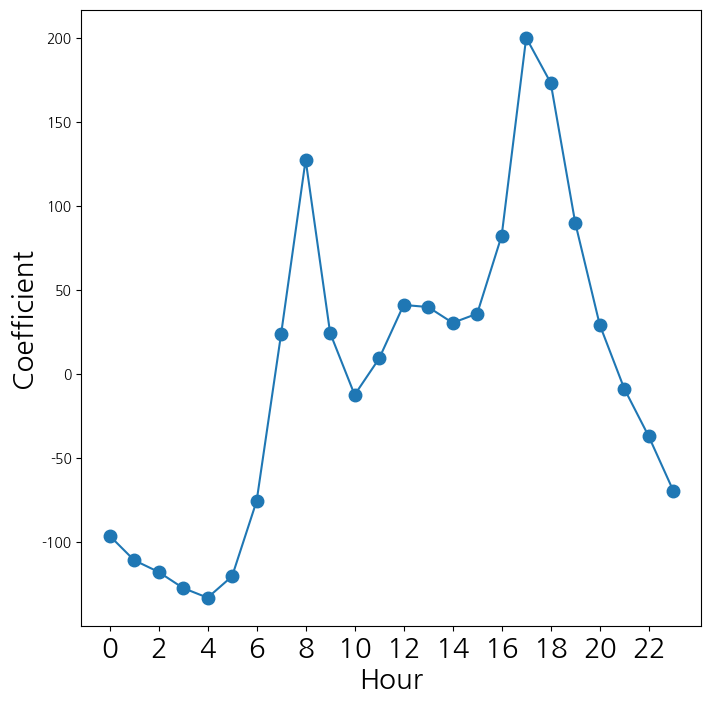

- 시간에 대응되는 계수들을 선도표로 연겨해서 시각화

coef_hr = S2[S2.index.str.contains('hr')]['coef']

coef_hr = coef_hr.reindex(['hr[{0}]'.format(h) for h in range(23)])

coef_hr = pd.concat([coef_hr, pd.Series([-coef_hr.sum()], index=['hr[23]'])

])

fig_hr , ax_hr = subplots(figsize=(8,8))

x_hr = np.arange(coef_hr.shape[0])

ax_hr.plot(x_hr , coef_hr , marker='o', ms=9)

ax_hr.set_xticks(x_hr[::2])

ax_hr.set_xticklabels(range(24)[::2], fontsize =20)

ax_hr.set_xlabel('Hour', fontsize=20)

ax_hr.set_ylabel('Coefficient', fontsize=20);